There are a lot of rumblings in the news about the current state of the labor markets. It can often be difficult and confusing to get to a clear picture in a world where a simple search yields seemingly contradictory results like “Labor Market Boom Cooled Some in 2022” and “Stock Futures Retreat After Strong Labor-Market Data”. Even if you click into those articles and read, it seems as though 2022 was “the second-best year for job creation” since 1940, but several large companies said they planned to lay off tens of thousands of workers through 2023. As a layman, or anyone short of Milton Friedman, it can be easy to become confused. That’s why, in this series, The Future of the Industrial Tech Workforce, Artemis will cut through the noise and breakdown what is happening and why, the impacts you can expect, and the solutions available to Industrial Tech business owners and entrepreneurs.

Before we begin, it is important to bring a baseline understanding to the conversation – especially around some of the more often cited economic statistics related to the overall job market and what is driving the issues. While the majority of this series relates to the current conditions and challenges plaguing the Industrial Tech labor market, today our focus will be on broader factors like cultural shifts impacting labor dynamics, the ongoing influence of COVID-19 related developments on the workforce and employers, and something not often thought of, Unemployment Rate vs Labor Force Participation Rate.

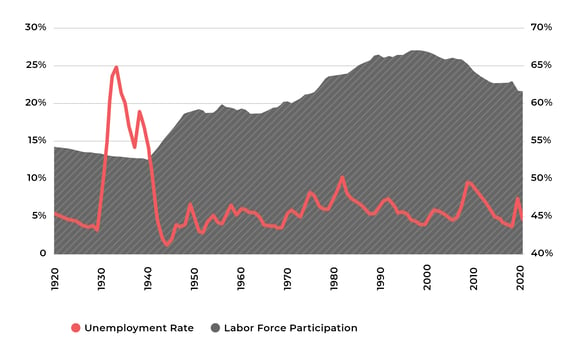

As a frame of reference, it makes sense to begin the conversation of unemployment and labor force participation in a period of American history – just before the calamitous years of the Great Depression and World War II – known as the Roaring Twenties. This was a period of rapid economic growth and heightened prosperity. In 1929, unemployment was 3.2%, inflation was .6%, and approximately 20-25% of the entire American workforce worked in Industrial and Manufacturing environments. On the heels of a near global conflict, American industry was booming in a way we hadn't seen before. Fast forward to today, manufacturing makes up a smaller and smaller portion of the labor force. That labor force participation has declined more than 6% in the last 20 years, and inflation has even the sharpest economists uncertain about what the next 24 months holds.

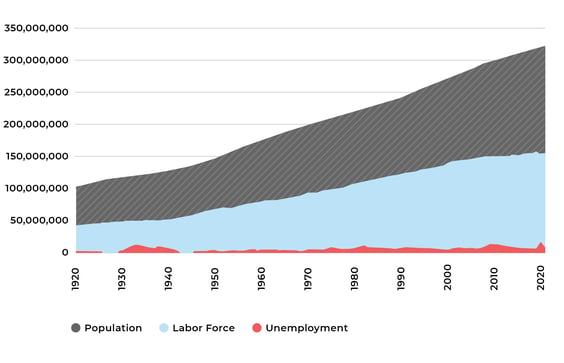

Focusing in on labor force participation and unemployment, the charts below relay the reality that – while the unemployment rate has continued to remain predictably between 3-15% - in the last 20 years, labor force participation has been consistently declining from its high of 67.11% (162.4 Million) in 1997 to the current 61.66% (160.0 Million) while the population has increased 17.6% from 282.1 Million to 331.8 Million.

This is widely considered to be a result of baby boomers leaving the workforce, exacerbated (gladly) by the increased life expectancy of aging generations, and an increased cultural expectation surrounding the attainment of higher education, delaying the entrance of workers into the workforce.

Let’s breakdown the information above more practically, so we can understand how important this data is. The difference between the population size and the labor market size, is the amount of people that are only contributing to the demand side of economic conditions. Think of it like this, everyone who is working is contributing in some way to the supply that the economy can offer while also contributing to the demand side through daily purchases. Everyone who is not working, however, is still making daily purchases, but isn’t generating supply. This is actually a good thing in strong economies, because more demand creates economic opportunity, but this is only true when there is a labor market capable of supporting economic growth and opportunism. When there is demand, but no ability for entrepreneurs, business owners, or large companies to generate supply, heightened inflation and a cadre of other negative economic implications can occur. Put frankly, if trends such as these continue, the long-term secular shock to industries and specific businesses could become increasingly problematic.

Only serving to further complicate this “potential” problem (scare quotes because it is already an issue in various industries), are a number of not necessarily economic developments. From the retirement of the Baby Boomer generation amounting to 10,000 per day to the recent growth in the importance of corporate social responsibility to American business, we as entrepreneurs and business owners are navigating relatively uncharted waters. It’s easy to recognize that, in the wake of the recent mass layoffs and cost-cutting in the tech industry, the companies that want to succeed will need to adopt innovative tactics if they intend to attract and keep top talent.

If you have participated in the economy in the last two years, it is likely that you have seen the impacts of the labor shortage on real life scenarios. From service declines as restaurant owners endure the mass exodus of employees from the industry to the impact of the labor shortage is the construction sector on the nation’s infrastructure plans, finding and retaining skilled and unskilled workers presents a serious challenge to widespread economic growth across sectors.

Lastly, and worthy of note, the immense impact of the COVID-19 pandemic on overall employee expectations cannot be understated. As the article relays: the workplace has changed, and it doesn’t show any signs of returning to the way it was before. With companies still adapting to the differences between the Generation X and Millennial demographics, employers are staring down the barrel of another generational shift alongside the growth of hybrid work schedules, DEI initiatives, the Great Resignation, and potentially even the expectation of reduced hours.

While these data points and cultural trends can be concerning, that is not the point of this series. We’re talking about this because, as business owners, we see it as a responsibility to our own customers and partners to be at the forefront of finding solutions and we think we can help other business owners do the same.

Over the weeks to come, we are going to be discussing the state of the Industrial Tech Workforce as it relates to the data in this piece and drilling down to explain the unique aspects of this sector and why we think the industry is offering a unique opportunity to be innovative and agile. We will end the series by offering up potential solutions that can be incorporated at the industry-wide and company level. Following that will be a 4 Part-Plan where we fully share a North-star playbook for business owners and entrepreneurs that are looking to get ahead of their competition.

Be sure to check back soon and let us know what else you’d like to hear from us. From macroeconomic trends to individual technological innovations, Artemis works continuously to stay at the forefront of the Industrial Tech frontier every day. Join us as we continue striving towards our vision of buying and building deeply impactful Industrial Tech businesses that enhance global health, security, and productivity.

-

Engineering Tomorrow: McDanel Optics For High-Performance Glass & Sapphire Solutions

Artemis industrial tech portfolio companies specialize in embedded technologies...

-

Engineering Tomorrow: McDanel Advanced Material Technologies

Artemis industrial tech portfolio companies specialize in embedded technologies...

-

Part 4: The Benefits and Wage Dilemma

In Part 4 of our Industrial Tech Skilled Labor Gap Playbook this week we introduce, The...