Last week, we discussed some of the prevailing secular trends in broader labor markets, the dynamics at play between a growing economy and shrinking labor force, and the major workplace and cultural shifts affecting the ability of employers to manage workforce expectations and availability. This week, we will be drilling down on how the broader trends referenced in Part 1 are specifically impacting the Industrial Tech Manufacturing industry, as well as some of the unique headwinds presenting significant challenges to manufacturers nationwide.

As you might recall, in Part 1 of this series, we opened with some daunting statistics around the overall decline of labor force participation. We highlighted the reality that – as unemployment has consistently fluctuated between 3-15% (with most years on the lower end of that spectrum, the actual real number of employees in the labor force has declined by 2.4 million in the same time that the population has increased by almost 50 million). These trends have what is called an inelastic impact on the manufacturing sector. Meaning that, as the situation worsens broadly, the pressure on manufacturing businesses will increase in even greater proportion.

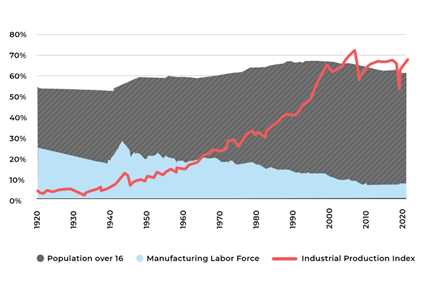

To put a point on this idea, in 1920 – 40 years after Thomas Edison’s light bulb – approximately 25% of the American workforce or 10 million people, worked in the manufacturing sector. As of September of 2022 there were 12.88 million manufacturing workers in the entirety of the United States. In that same time, the Industrial Production Index (“IPI”) – which measures the real output in terms of percentage difference - shows that the total output of this sector of the economy has increased almost 18 times due to technological advances increasing individual worker productivity. However, despite these trends, productivity innovation in the manufacturing sector is no longer outpacing the percentage decline in manufacturing workers. This leads to what we see in the chart below. It demonstrates the correlation between the stagnation of overall labor force growth and the shrinking manufacturing labor force to the flatlining manufacturing production over the past 25 years.

Alright, now that we got the boring (if slightly terrifying) statistics out of the way, we can wake up and start to make practical sense of all this data. The correlation between these data points indicates that the impact of a shrinking overall labor force coupled by a smaller and smaller portion of that labor force available to the manufacturing sector, is manifesting itself in the form of a major depression of the long-term growth rate of manufacturing output. Put plainly, it is very likely that – if these trends continue – that the manufacturing industry as whole will see a severe decline in its ability to create goods over the next 10-25 years.

With that said, there is one trend that is likely providing the buoyancy that we are currently seeing in the Industrial Production Index (IPI). The widespread adoption of advanced automation technologies has dramatically increased the productivity of each individual worker as evidenced inherently in the IPI vs Manufacturing Labor Force numbers. Though, this pattern was offset by recent 10 year headwinds that have reversed the 1980-2010 norm, where productivity per worker more than doubled. This indicates that labor productivity – or the real economic output per labor hour – declined by over 5% between 2012 and 2020. All of this to say that, having technology as the only or primary value lever being pulled is potentially dangerous to the industry when technological innovation lags. However, technology remains a useful tool for both leadership and labor to boost productivity, increase individual and corporate earnings, and advance innovation.

Across the manufacturing industry, the growing dependency on various automation technologies within the manufacturing process is leading to a decrease in the number of unskilled employment opportunities and drastic exacerbation of a skilled labor shortage. As Deloitte’s study relays, the manufacturing industry lost nearly six years of bull market job gains during the 2020 Covid-19 Pandemic and predicts that – by 2030 – the industry will be operating with 2.1 million unfilled jobs (equating to approximately $1 Trillion in unrealized production).

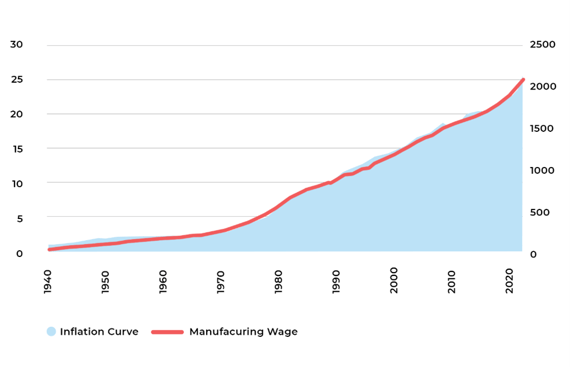

Many factors only further complicating these circumstances range from (i) the Great Resignation – a new workforce dynamic impacting manufacturing with unique prejudice – and (ii) a desire for more flexible schedules to (iii) the recent lagging of wages for nonsupervisory roles (i.e. manufacturing production positions) – despite the long-term consistency of manufacturing wages against inflation seen in the chart below – and (iv) a general misconception by the American public about the safety, technological sophistication, and career advancement opportunities that are prevalent across the manufacturing industry.

While these data points and cultural trends can be discouraging, that is not the point of this series. We’re talking about this because, as business owners, we see it as a responsibility to our own customers and partners to be at the forefront of finding solutions – and we think we can help business owners do the same.

In the coming weeks, we are going to be drilling down to explain the unique aspects of the Industrial Tech labor force and why we think the industry is offering a unique opportunity to be innovative and agile, providing potential solutions that can be incorporated at the industry-wide and company level, and wrapping it all up with a Multi-Part Playbook for business owners and entrepreneurs that are looking to get ahead of their competition.

Be sure to check back and let us know what else you’d like to hear from us, as we continue striving towards our vision of buying and building deeply impactful Industrial Tech businesses that enhance global health, security, and productivity.

-

Engineering Tomorrow: McDanel Optics For High-Performance Glass & Sapphire Solutions

Artemis industrial tech portfolio companies specialize in embedded technologies...

-

Engineering Tomorrow: McDanel Advanced Material Technologies

Artemis industrial tech portfolio companies specialize in embedded technologies...

-

Part 4: The Benefits and Wage Dilemma

In Part 4 of our Industrial Tech Skilled Labor Gap Playbook this week we introduce, The...